Public Bank Stock Performance – February 2020

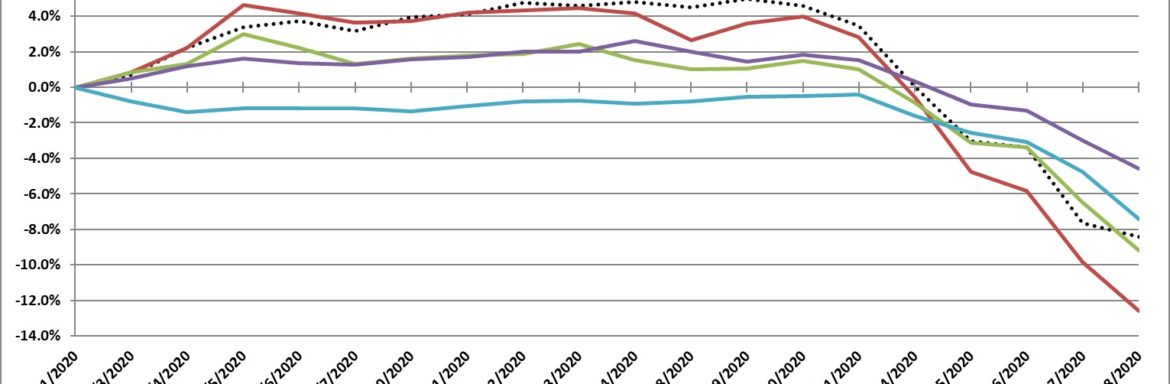

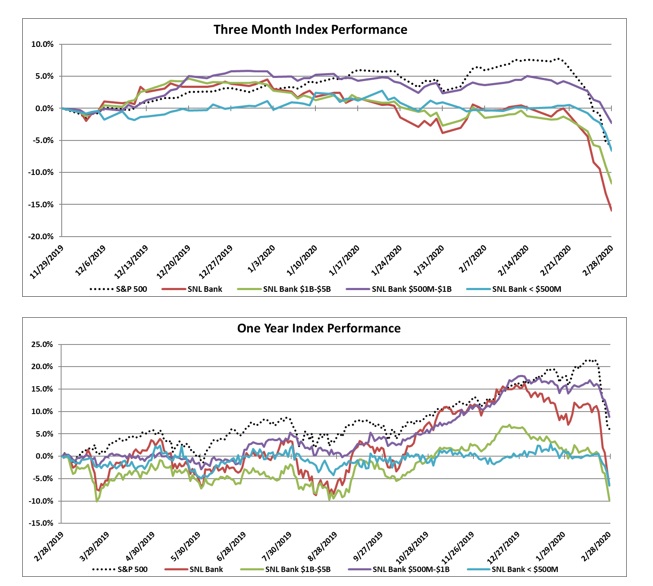

In the month of February, the S&P 500 outperformed the SNL Bank Index, with a decrease of 8.4% compared to a decrease of 12.6% for the SNL Bank Index. Stocks were volatile during the month of February as fears surrounding the coronavirus overtook investor sentiment.

After a positive start to the month, stocks fell sharply in response to growing uncertainties about the impact of the coronavirus on economies and companies around the world. In early February, stocks were rising strongly, boosted by positive economic news. Then on Friday, February 21st, there was news of an increase in the number of people infected by the coronavirus in South Korea, and investors realized that the virus posed global threats. Bond prices rose as investors moved to less risky assets. With little known for certain, markets reacted strongly to any news about the virus. The uncertainty continues, and markets will likely continue to be volatile.

Recession fears have increased as the Federal Reserve continues to drop rates. The interest rate targeted by the Federal Reserve, the range of the federal funds rate, is currently 1.0% to 1.25%. This is the range after the Fed cut it half of a percentage point on March 3, 2020. It was the first rate cut in 2020, following three rate cuts in 2019, and came in response to the threat posed to the economy by the coronavirus.

In economic news, data from the U.S. Department of Labor reported that nonfarm payrolls increased by 273,000 in February, compared with forecasts for an increase of 175,000. The unemployment rate edged lower to 3.5%, while average hourly earnings increased by 3.0% year over year. Excluding government hiring, private payrolls grew by 183,000 in February, exceeding Dow Jones estimates for 155,000. In January, U.S. existing-home sales declined 1.3% from December. The median existing-home price for all housing types in January was $266,300, up 6.8% from January 2019. January’s price increase marks the 95th straight month of year-over-year gains.

Bank M&A pricing was down in February 2020 compared to February 2019 on a fewer number of transactions Click here for February 2020 M&A Transactions

The SNL Bank Index showed an overall decrease through the month dropping 12.6%, compared to the S&P 500 which was down 8.4%. The SNL Bank Index was down in the larger size groups as banks between $1 billion and $5 billion decreased 9.2%, banks between $500 million and $1 billion decreased 4.6%, and banks below $500 decreased 7.4%.

Over the three-month period ending February 2020, the SNL Bank Index decreased 15.9% while the S&P 500 decreased 5.9%. Over the prior twelve months, the SNL Bank Index decreased 6.5% while the S&P 500 increased 6.1%. Banks between $1 billion and $5 billion decreased 9.7%, banks between $500 million and $1 billion increased 8.8%, and banks with assets less than $500 million decreased 6.6%.

REGIONAL PRICING HIGHLIGHTS

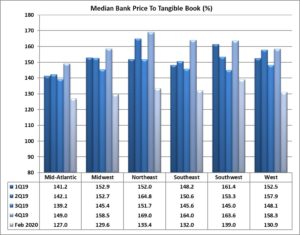

In February, pricing was down across all six regions. The West experienced the largest decrease since January of 11.8%, falling to the third lowest priced region with a price to tangible book multiple of 130.9%. The Southwest remained the highest priced region at 139.0% price to tangible book after decreasing by 9.1% in the month. The Northeast and Southeast decreased 10.9% and 10.4%, respectively, to a price to tangible book of 133.4% and 132.0%, respectively. The Midwest saw an 8.5% decrease to a price to tangible book of 129.6%, while the Mid-Atlantic was the lowest priced region on a price to tangible book multiple of 127.0%.

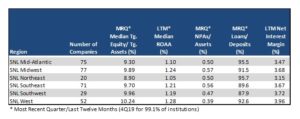

The West remained the most profitable region with an ROAA of 1.28% and had the best NIM of 3.96%, the strongest asset quality (NPAs/Assets 0.39%), and stable loan demand with Loans/Deposits of 92.6%. The Midwest was the second lowest priced region, but was the second highest in profitability (ROAA of 1.24%) and had NIM of 3.68%. The Northeast region’s asset quality has improved since December (NPAs/Assets of 0.50% from 0.58%) and the region remained the highest in loan demand (Loan/Deposits of 95.7%). The Southwest region had the second strongest NIM of 3.72% and the fourth strongest profitability with an ROAA of 1.19%.

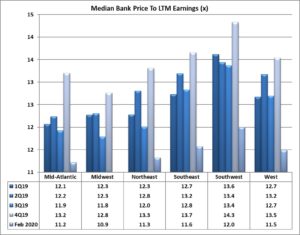

On a median price to earnings basis, pricing decreased across all of the six regions. The Southwest region decreased 8.0%, but remains the highest priced region with a price to earnings multiple of 12.0x. The Southeast and West decreased 10.3% and 7.0%, respectively, to a price to earnings multiple of 11.6x and 11.5x, representing the second and third highest priced regions, respectively. The Mid-Atlantic saw a decrease of 9.0% in February to a price to earnings multiple of 11.2x. The Midwest and Northeast decreased by 9.0% and 6.7%, respectively, in February to a price to earnings multiple of 10.9x and 11.3x, respectively (representing the lowest and third lowest priced region).

PRICING BY SIZE

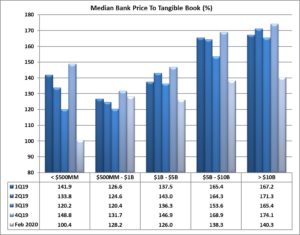

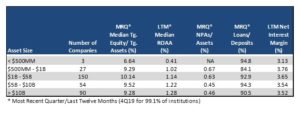

Size continues to impact bank stock prices. Financial institutions with total assets greater than $1 billion consistently report substantially higher median price to tangible book pricing than their peers with total assets less than $1 billion. In the month of February, that differential was 21.0% higher for the peers with assets greater than $1 billion on a price to tangible book basis. The second highest priced asset class remained the group with assets between $5 billion and $10 billion, which experienced a decrease in pricing of 11.4% to a 138.3% price to tangible book multiple, below the 140.3% multiple of the banks greater than $10 billion which decreased by 12.9%. The group with assets from $1 billion to $5 billion decreased by 6.7% to a price to tangible book multiple of 126.0%. The group with assets from $500 million to $1 billion and the group with less than $500 million (which constitutes only three companies) ended the month with price to tangible book multiples of 128.2% and 100.4%, respectively, with pricing for the $500 million to $1 billion group decreasing 2.6% while the group less than $500 million decreased by 2.9%.

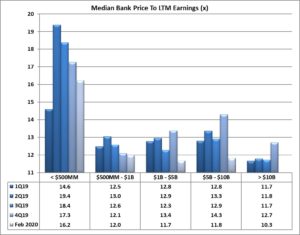

On a price to LTM earnings basis, the largest bank group (over $10 billion) saw a decrease in pricing of 12.7%. The group with assets between $500 million and $1 billion saw the smallest decrease in its price to earnings multiple, down 0.7% to 12.0x. The group with assets between $1 billion and $5 billion saw a decrease of 6.3% to a price to earnings multiple of 11.7x (the second lowest among the groups), while the group between $5 billion and $10 billion saw a decrease in pricing by 10.9% to a price earnings multiple of 11.8x. The asset group with less than $500 million assets remained the highest priced with a price to earnings multiple of 16.2x.

Financial institutions under $1 billion reported much lower LTM ROAA (average of medians 0.71%) and loan demand (average Loans/Deposits of 89.4%) than institutions with assets over $1 billion (average of median LTM ROAA of 1.22% and Loans/Deposits of 92.9%).

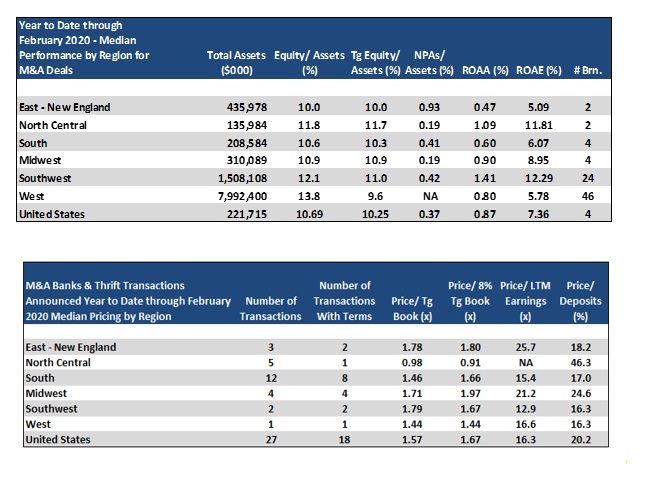

Mergers & Acquisitions by Region

Bank consolidation was down slightly in February 2020 as compared to February 2019 with 27 transactions announced in February 2020 (18 transactions with terms) compared to 34 transactions (15 with terms) in February 2019. Median YTD pricing in February 2020 was lower than 2019 on a price to tangible book decrease of 1.8% (median 1.57x), a price to 8% tangible book increase of 3.2% (1.67x), an increase of price to deposits of 14.8% (20.2%), and a price to earnings basis with a 2.8% decrease on LTM earnings (16.3x).

The South region had the highest number of transactions with twelve deals through February of which eight reported terms. The North Central region logged five transactions (one with terms) with the lowest price to tangible book multiple of 98% but the highest price to deposits of 46.3%. Transactions in the Southwest reported the highest price to tangible book of the group with a multiple of 179%. There were four transactions in the Midwest and only one transaction in the West with price to tangible book multiples of 171% and 144%, respectively. The East region saw three transactions in the first two months of 2020 with the second highest price to tangible book multiple of 178%.

Click here to view all transactions announced in February 2020